Home » Archives

Peraturan perundang-undangan tentang pengangkutan laut

- Wednesday, December 29, 2010, 9:17

- International Convention, Maritime Convention, Pelayaran

- 2 comments

Please click for downloading

Undang-Undang dan Peraturan

a) UU No.17 Tahun 2008 Tentang Pelayaran

b) PP No.61 Tahun 2009 Tentang Kepelabuhanan

c) PP No.20 Tahun 2010 Tentang Angkutan di Perairan

d) KM No.14 Tahun 2002 Tentang Penyelenggaraan dan Pengusahaan Bongkar Muat Barang dari dan ke Kapal

Full story

Tanggung Jawab Pengangkut (Tidak Jelas)

- Tuesday, December 28, 2010, 9:33

- Pelayaran

- 2 comments

")

Proposal Training: “Hull & Machinery (H&M)” dan “Protection & Indemnity (P&I)”

- Saturday, December 25, 2010, 15:19

- Marine Insurance, Training

- 2 comments

Download : Proposal Training for details

proposal-training-hm-and-pi1

Isi Materi (Contents)

Jenis-jenis asuransi kapal

a) Asuransi Lambung dan Mesin Kapal (Hull & Machinery)

b) Asuransi Tanggung Jawab Hukum Pengoperasian Kapal (Protection & Indemnity)

c) Asuransi Tanggung Jawab Hukum Pihak Pen-charter (Charterers Liability)

d) Asuransi Pembangunan Kapal (Builders Risks)

Full story

Proposal Training “Marine Cargo Insurance”

- Saturday, December 25, 2010, 10:56

- Marine Insurance, Training

- 3 comments

Isi Materi (Contents)

Institute Cargo Clauses (ICC (A), (B) dan (C))

a) Risks Covered (Risiko yang dijamin)

b) General Average Clause

c) Collision Liability

d) General Exclusions (Risiko yang tidak dijamin)

e) Unseaworthiness and Unfitness Exclusion

f) War & Strikes Exclusion

g) Duration of Cover (Transit)

h) Insurable Interest

Full story

Prinsip Tanggung Jawab Dalam Pengangkutan

- Tuesday, December 21, 2010, 9:12

- Freight Forwarders Liability, Freight Forwarders Liability

- Add a comment

1. Prinsip tanggung jawab berdasarkan kesalahan (fault liability)

2. Prinsip tanggung jawab berdasarkan praduga (presumption of liability)

3. Prinsip tanggung jawab mutlak (absolute / strict liability)

Full story

What is a Bill of Lading?

- Tuesday, December 21, 2010, 9:05

- Freight Forwarders Liability, Freight Forwarders Liability

- 1 comment

{kind=link}

Cargo Liability

- Saturday, September 25, 2010, 9:32

- Protection & Indemnity, Protection & Indemnity (P&I)

- 4 comments

Jaminan kerugian, kerusakan atau kekurangan barang muatan (Cargo Liability) adalah salah satu jenis jaminan dalam polis Protection & Indemnity (P&I). Jaminan Cargo Liability sangat penting terutama untuk jenis kapal barang seperti Cargo ships, Tankers, maupun Barges dan kapal-kapal lainnya yang memuat kargo milik pihak ketiga. Full story

{kind=link}

Penahanan dan Penyitaan Kapal

- Saturday, September 25, 2010, 9:27

- Protection & Indemnity, Protection & Indemnity (P&I)

- Add a comment

Penyitaan kapal dapat bersifat sementara berupa penundaan keberangkatan kapal disuatu pelabuhan tertentu ataupun dapat berupa sita tetap atas kapal maupun muatannya. Dapat dibayangkan, apabila terjadi penahanan kapal – walau hanya sehari, maka biaya opearsional yang dikeluarkan akan sangat mahal. Bahkan melebihi nilai klaim yang dituntut. Full story

Multy Fanny Ajukan 16 Bukti Perkuat Gugatan ke Asuransi Tugu

- Saturday, August 14, 2010, 18:01

- Insurance News

- 2 comments

JAKARTA. Sidang gugatan terkait klaim pembayaran asuransi kapal yang dilayangkan PT Multy Fany Bahari Sea Shore kepada PT Asuransi Tugu Kresna Pratama kembali digelar. Kali ini sidang memasuki tahap pembuktian gugatan. Full story

Gebrakan Pemegang Saham Minoritas

- Tuesday, August 10, 2010, 11:03

- Insurance News

- 1 comment

Dituduh menerbitkan obligasi tak sesuai dengan aturan, PT Hero Pusaka Sejati “pemegang saham mayoritas Hero Supermarket”dituntut Rp 210 miliar.

Dairy Farm hendaknya menyimpan dulu ambisinya untuk menguasai PT Hero Supermarket Tbk. Penyebabnya, PT Hero Pusaka Sejati ”pemegang saham mayoritas Hero Supermarket”Jumat dua pekan silam dituntut Rp 210 miliar oleh PT Matahari Putra Prima Tbk. Penerbitan obligasi oleh Hero Pusaka Sejati senilai US$ 36,4 juta yang bisa dikonversi menjadi 24,55% saham dianggap menabrak aturan. Full story

Eksepsi Tergugat Dikabulkan, Gugatan MandiriRe Kandas

- Tuesday, August 10, 2010, 11:00

- Insurance News

- Add a comment

Saat sidang berlangsung hingga putusan dibacakan Marine and General Underwriting Ltd dan Crawley Warren International Ltd tak hadir di pengadilan.

PT MandiriRe International harus menelan pil pahit. Perusahaan jasa pialang asuransi itu tak berhasil menuntut Marine and General Underwriting Ltd membayar klaim PT Asuransi Ramayana senilai Rp14,8 miliar. Full story

Perusahaan Asuransi Ngotot Tolak Klaim Asuransi PT Pelayaran Manalagi

- Tuesday, August 10, 2010, 10:58

- Insurance News

- Add a comment

Kamis, 17 Juni 2010, hukumonline - Sebab PT Pelayaran Manalagi dinilai melakukan perbuatan melawan hukum dengan mengangkut barang berbahaya yang mudah terbakar.

PT Asuransi Harta Aman Pratama Tbk keukeuh menolak klaim asuransi PT Pelayaran Manalagi. Alasan-alasan yang diutarakan PT Pelayaran Manalagi dalam gugatan tidak mengubah pendirian perusahaan asuransi itu. Full story

Hati-hati, Beragam Modus Penipuan Asuransi

- Wednesday, August 4, 2010, 22:59

- Insurance News

- 4 comments

Normal 0 < !-->"Nomor mesin mobil dan nomor rangka mobil dipotong lalu dlmutasikan ke kendaraan bermotor yang lain," tutur Petrus pada acara Dialog Eksklusif Warta Kota bertema Cara Mudah Mengurus Klaim Asuransi di Gedung Kompas-Gramedia, Palmerah Barat, Selasa Selain Itu, ada Juga penipuan asuransi yang terjadi dengan mengajukan laporan kehilangan kendaraannya untuk mendapatkan dana asuransi, padahal motor atau mobilnya tidak hilang. Oknum nasabah asuransi itu mendapat dana klaim asuransi dari perusahaan asuransi dan kendaraannya tetap berada di tangannya. Nasabah itu lalu memalsu BPKB mobil barunya itu untuk mengajukan polis asuransi di perusahaan asuransi lain. Full story

Sandiwara Di Masalembo

- Wednesday, August 4, 2010, 22:45

- Insurance News

- 1 comment

02 Januari 1982; PERAIRAN Masalembo? Nama ini mengingatkan kita kepada kematian. Lintas laut ini, yang paling ramai bagi kapal yang pulang pergi antara Jawa dengan Kalimantan dan Sulawesi, ternyata memang merupakan "Segi Tiga Bermuda" Indonesia. Full story

Kejahatan Asuransi Mati Dalam Asuransi Sebuah Modus…

- Wednesday, August 4, 2010, 22:34

- Insurance News

- 2 comments

02 Januari 1982; SESOSOK mayat membusuk ditemukan di semak-semak pinggir jalan raya dekat Desa Sambirejo, Kendal, Jawa Tengah. Sebuah peluru bersarang di batok kepalanya dan sebuah lagi menembus mulut sampai kuping kiri. Full story

PK MA kukuhkan kendaraan hilang tanggung jawab pengelola parkir

- Thursday, July 29, 2010, 10:48

- Car Insurance, Insurance News

- Add a comment

Jakarta - Mahkamah Agung (MA) mengukuhkan tanggung jawab ganti kerugian dari pengelola jasa perparkiran bagi konsumen yang kehilangan kendaraan di tempat parkir.

Diketahui, permohonan peninjauan kembali (PK) secure parking PT Securindo Packatama Indonesia ditolak terkait gugatan Anny R Gultom dan Hontas Tambunan yang kehilangan mobil Kijang Super tahun 1994 pada 1 Maret 2000, di Plaza Cempaka Mas. Full story

Secure Parking bersedia laksanakan putusan PK MA

- Thursday, July 29, 2010, 10:33

- Car Insurance, Insurance News

- Add a comment

Konsumen Menang Lawan Secure Parking

- Thursday, July 29, 2010, 10:23

- Car Insurance, Insurance News

- Add a comment

JAKARTA, KOMPAS.com — Gugatan yang dilayangkan Andi Tjandra, konsumen yang kehilangan mobil Honda CRV saat melakukan parkir di Wisma Nusantara, kepada PT Securindo Packtama atau Secure Parking dikabulkan Pengadilan Negeri Jakarta Pusat. Andi adalah konsumen yang kehilangan mobil Honda CRV warna abu-abu muda metalik dengan nomor polisi B 1008 WX. Full story

Perils vs Hazards?

- Thursday, July 15, 2010, 6:40

- Risk Management

- 4 comments

Sering orang mempersamakan pengertian Risiko dengan Peril dan Hazard. Memang ketiga istilah tersebut berkaitan erat satu sama lain akan tetapi berbeda dalam pengertian. Peril adalah suatu peristiwa yang dapat menimbulkan kerugian, sedangkan Hazard adalah keadaan yang dapat memperbesar kemungkinan terjadinya suatu peril. Full story

What is a Risk?

- Thursday, July 15, 2010, 6:27

- Risk Management

- Add a comment

Risiko sendiri juga merupakan inti dari pada kehidupan itu sendiri, sehingga banyak orang dengan latar belakang yang berbeda sangat memperhatikan masalah ini. Ekonom, Dokter, Psykologis, Pengusaha, llmuwan dan lainnya mempunyai kepentingan dalam konsep risiko, sehingga sudah banyak definisi-definisi risiko yang diperkenalkan oleh para ilmuwan tersebut, seperti tercantum di bawah ini: Full story

Collision and Non Contact Incidents

- Wednesday, June 2, 2010, 22:38

- Hull & Machinery

- Add a comment

Introduction

Collision is one of the few areas where third party liabilities may be covered by the hull policy. Traditionally, the English hull policy covered 3/4ths of the collision risks and the P&I Clubs the remaining 1/4th. Full story

Fixed and Floating Objects (FFO)

- Wednesday, June 2, 2010, 22:17

- Hull & Machinery, Protection & Indemnity (P&I)

- Add a comment

Under the Rules of the Club, cover of a vessel’s liabilities for loss of, damage to, or interference with rights in relation to any fixed or moveable property whether on or above, in or below land or water. Full story

What is a 3/4th Collision Liability?

- Wednesday, June 2, 2010, 22:07

- Hull & Machinery, Hull & Machinery (H&M)

- 13 comments

Assume that both vessels in an example collision are insured for 3/4th collision liability with their hull underwriters and for 1/4th with their P&I Clubs. In the example vessel A is 75% to blame for the collision and vessel B is 25% to blame. Full story

Piracy update – EU Council Regulation 356/2010

- Tuesday, May 18, 2010, 23:40

- Insurance News

- Add a comment

Further to our update below, we are aware that the EU Council regulation no 356/2010 entered into force on the 28th April. It adopts similar provisions to the US Executive Order prohibiting payments to certain parties linked with Somalia and is directly applicable, in other words it will apply in EU states without the need for any national implementation.

Full story

Australian Bank Fees Targeted in Massive Class Action

- Tuesday, May 18, 2010, 23:31

- Liability Casualty

- Add a comment

Proposed suits highlight the role being played in the Australian class action market by IMF Ltd., a publicly traded litigation funding company that is basically bankrolling the bank suits Full story

Korban Kecelakaan Tabung LPG 3 Kg Bisa Klaim Asuransi

- Monday, May 17, 2010, 9:34

- Insurance News

- 4 comments

{kind=link}

Harga kapal tongkang naik 16,6%

- Thursday, May 13, 2010, 7:05

- Insurance News

- 1 comment

JAKARTA (Bisnis.com): Kenaikan harga kapal tongkang sebesar 16,6% akibat lonjakan harga baja belum berpengaruh terhadap rencana perusahaan pelayaran nasional untuk melakukan pengadaan armada jenis ini.

Full story

Legal Cost & Expenses Cover for Ship Owners / Operators

- Tuesday, May 11, 2010, 14:38

- Protection & Indemnity

- Add a comment

Subject to the direction and discretion of the Underwriter, the Assured shall be indemnified by the Underwriter against its reasonable costs and expenses, arising from event occurring during occurring the Period of Insurance and incurred by the Assured in respect of the operation of the Insured Vessel.

Full story

Charterers Liability Cover

- Sunday, May 9, 2010, 17:02

- All Quotes, Charterers Liability

- 2 comments

Protection & Indemnity Cover

- Sunday, May 9, 2010, 16:57

- Protection & Indemnity (P&I)

- 5 comments

The underwriter shall indemnify the Assured against those liabilities, losses, costs and expenses, arising from events occurring during the Period of Insurance and incurred by the Assured in respect of the operation of the Insured Vessel. Full story

Apa keuntungan “Fixed Premium P&I” dibandingkan dengan “Mutual P&I Club”?

- Tuesday, April 20, 2010, 10:32

- Protection & Indemnity, Protection & Indemnity (P&I)

- 3 comments

Selama lebih dari 100 tahun P&I Club adalah satu-satunya yang menyediakan jaminan Protection & Indemnity namun kini juga telah hadir jaminan P&I yang diberikan oleh perusahan Asuransi yang disebut Fixed Premium P&I

Full story

Hull & Machinery (H&M)

- Thursday, April 8, 2010, 22:30

- All Quotes, Hull & Machinery (H&M)

- 23 comments

")

{kind=link}

Coverage for Claims Between the Named Insured and the Additional Insured (Cross Liability in CGL Policy)

- Friday, April 2, 2010, 23:37

- General Liability, General Liability (CGL), Liability Casualty

- 1 comment

Sometimes the Additional Insured misunderstands the nature of coverage bestowed by an Additional Insured endorsement. Sometimes too the insurer misunderstands the separate nature of the coverage provided to the Additional Insured for certain claims. Full story

Additional Insureds and Policy Exclusions (in CGL Policy)

- Thursday, April 1, 2010, 7:12

- General Liability, General Liability (CGL), Liability Casualty

- Add a comment

In Stolberg v. Pearl Assurance Co. S.C.R. 1026, three construction companies were the Named Insured under a CGL policy and the president of the companies was added to coverage by way of a separate endorsement which read: Full story

Apa yang dimaksud dengan Total Loss dalam Asuransi Kapal (Hull & Machinery)?

- Wednesday, March 31, 2010, 9:09

- Hull & Machinery, Hull & Machinery (H&M)

- 12 comments

?")

{kind=link}

Association Liability Insurance – What, Why, When, Where & How?

- Thursday, March 25, 2010, 23:15

- Directors & Officers (D&O)

- 2 comments

{kind=link}

[Who] may claims against Directors and Officers?

- Sunday, March 21, 2010, 10:53

- Directors & Officers (D&O), Directors and Officers Liability, Liability Casualty

- Add a comment

![[Who] may claims against Directors and Officers?](https://ahliasuransi.com/wp-content/themes/wp-max100/scripts/phpThumb/phpThumb.php?src=https%3A%2F%2Fahliasuransi.com%2Fwp-content%2Fuploads%2F2010%2F03%2Fbankrupt.jpg&w=120&h=100&zc=T&q=95 "[Who] may claims against Directors and Officers?")

{kind=link}

Directors’ and Officers’ (D&O) Liability Insurance – Apa & Mengapa?

- Sunday, March 21, 2010, 10:10

- All Quotes, Directors & Officers (D&O)

- 4 comments

Liability Insurance - Apa & Mengapa?")

{kind=link}

Professional Indemnity Insurance (PI) – What, Why & How?

- Sunday, March 21, 2010, 9:31

- Professional Indemnity, Professional Indemnity (PI)

- Add a comment

– What, Why & How?")

{kind=link}

Professional Indemnity Insurance (PI) – Apa & Mengapa?

- Tuesday, March 16, 2010, 16:27

- Professional Indemnity, Professional Indemnity (PI)

- 6 comments

– Apa & Mengapa?")

{kind=link}

Professional harusnya Professional

- Tuesday, March 16, 2010, 16:06

- Professional Indemnity, Professional Indemnity, Professional Indemnity (PI)

- Add a comment

{kind=link}

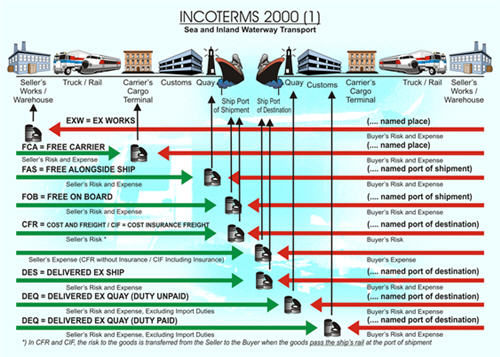

Incoterms

- Monday, March 8, 2010, 13:40

- Marine Cargo

- 3 comments

{kind=link}

Freight Forwarders’ Liability Insurance : Apa & Mengapa?

- Monday, March 1, 2010, 20:48

- All Quotes, Freight Forwarders Liability

- 22 comments

Piracy – ransom payments not contrary to public policy/recoverable as sue & labour under English Law

- Wednesday, February 24, 2010, 10:33

- Insurance News, Maritime Casualty

- Add a comment

The subject of piracy has been the subject of much debate given the numerous hijackings off Somalia and elsewhere over the last 18 months or so.

As far as we are aware, none of these cases have resulted in any decisions in the English Courts until the recent decision from the High Court in Masefield AG v Amlin Corporate Member Ltd.

Full story

What is sudden and unforeseen damage?

- Tuesday, February 23, 2010, 7:48

- Property Insurance

- 1 comment

Many insured companies have grappled with what is sudden and unforeseen damage, especially in business interruption and machinery breakdown policies. Various insurers have had to explain to unhappy clients that a claim was not covered by the insurance policy, because the damage was caused by normal wear and tear or another gradual cause, and was not sudden and unforeseen.

Full story

Siapa yang harus bertanggung jawab jika terjadi malpraktek? Dokter atau RS?

- Friday, February 19, 2010, 16:26

- Medical Malpractice, Medical Malpractice

- 1 comment

Menyambung tulisan sebelumnya RS tidak perlu takut malpraktek sudah dijelaskan mengenai pentingnya Medical Malpractice Insurance. Lalu siapa yang harus bertanggung jawab jika terjadi malpraktek? Dokter atau RS? Dalam hubungannya dengan Asuransi Medical Malpractice, Pertanyaan ini sama pentingnya dengan “Siapa yang perlu Asuransi Medical Malpractice? Dokter atau RS?

Siapa yang perlu Asuransi Medical Malpractice? Dokter atau RS?

Full story

RS tidak perlu takut malpraktek

- Thursday, February 18, 2010, 10:09

- Medical Malpractice

- Add a comment

{kind=link}

Robert Tantular dan Asuransi D&O (Directors & Officers) Liability

- Tuesday, February 16, 2010, 20:31

- Directors & Officers (D&O), Directors and Officers Liability

- Add a comment

Liability")

{kind=link}

AAUI genjot sertifikasi agen asuransi umum

- Tuesday, February 16, 2010, 20:22

- Insurance News

- 12 comments

JAKARTA (Bisnis.com): Asosiasi Asuransi Umum Indonesia (AAUI) terus menggenjot sertifikasi agen asuransi umum dengan menggelar ujian di Jakarta dan Semarang dalam waktu dekat ini.

Sektor asuransi umum terus mengejar ketertinggalannya dari sektor asuransi jiwa dalam hal penanganan agen. AAUI mulai tahun lalu menggenjot ujian keagenan yang hingga akhir tahun sudah berhasil menghasilkan 2.800 agen berlisensi.

Full story

Mengapa kami butuh Asuransi Liability?

- Monday, February 15, 2010, 13:36

- General Liability, General Liability (CGL)

- 4 comments

Mengapa kami butuh Asuransi Liability? Padahal pekerjaan kami hampir tidak mengandung risiko?

Itulah pertanyaan beberapa klien ketika mereka dipersyaratkan untuk membeli Asuransi Liability, pertanyaan itu menyiratkan dua hal, pertama bagi klien mereka tidak mengerti pentingnya Asuransi Liability, kedua bagi perusahaan Asuransi adalah tidak mudah menjual produk Asuransi Liability di Indonesia karena klien baru membelinya ketika ada persyaratan kontrak bukan karena suatu kebutuhan.

Full story

Seandainya mereka tahu Asuransi itu murah dan mudah?

- Monday, February 15, 2010, 13:32

- Learn More

- 1 comment

Hampir tidak ada kegiatan ekonomi dewasa ini bisa berjalan tanpa “Asuransi”.

Tidak ada export-import tanpa polis Asuransi,

Kredit tidak bisa disalurkan tanpa Asuransi,

Tidak ada pembangunan gedung, jembatan dan infrastruktur tanpa Asuransi,

Kapal (seharusnya) tidak bisa berlayar tanpa polis Asuransi,

Mobil (seharusnya) tidak bisa berjalan tanpa bensin dan polis Asuransi,

Dokter (seharusnya) tidak bisa praktek tanpa polis Asuransi,

Direktur dan Komisaris (seharusnya) tidak bisa menjabat tanpa polis Asuransi,

Buruh-buruh (semestinya) tidak boleh bekerja tanpa polis Asuransi,

Rumah-rumah pun (seharusnya) tidak boleh dihuni tanpa polis asuransi,

Apalagi…??

Mengapa demikian?

Full story

Kegiatan usaha 10 pialang asuransi dibatasi

- Tuesday, February 9, 2010, 10:09

- Insurance News

- Add a comment

JAKARTA (bisnis.com): Biro Perasuransian Bapepam-LK mengenakan sanksi pembatasan kegiatan usaha kepada 10 perusahaan pialang yang tersangkut masalah aturan permodalan minimum Rp1 miliar.

Selain itu, sembilan perusahaan tercatat dikenakan sanksi peringatan ketiga.

Data Biro Perasuransian per 28 Januari menunjukkan 21 perusahaan pialang asuransi dan satu perusahaan pialang reasuransi belum memenuhi ketentuan modal minimum.

Full story

Bapepam-LK tak buat aturan tarif premi per produk

- Tuesday, February 9, 2010, 10:07

- Insurance News

- Add a comment

JAKARTA (Bisnis.com): Biro Perasuransian Bapepam-LK menegaskan regulator tidak akan membuat aturan cara menentukan tarif premi per produk untuk mengatasi perang tarif di industri asuransi kerugian.

Kepala Biro Perasuransian Bapepam-LK Isa Rachmatarwata mengatakan pembuatan aturan per produk sangat menyita waktu dan tidak menimbulkan kedewasaan pelaku, karena pada dasarnya aturan untuk menentukan premi sudah ada di KMK 422/2003 tentang Penyelenggaraan Usaha Perusahaan Asuransi dan Reasuransi.

Full story

Biaya Recall Toyota USD2 M

- Monday, February 8, 2010, 11:41

- Insurance News

- Add a comment

TOKYO (SI) – Toyota Motor Corporation menyatakan telah menyiapkan dana 180 miliar yen (USD2 miliar) untuk penarikan kembali (recall) delapan juta unit kendaraan di seluruh dunia.

Toyota akan memberi dana USD75.000 untuk setiap dealer di Amerika Serikat (AS) sebagai biaya perbaikan delapan model yang ditarik kembali. “Dalam beberapa hari,Anda (dealer) akan menerima cek dari kita untuk perbaikan kendaraan konsumen Toyota,” kata Vice President Toyota Bob Carter dalam surat yang dikirim ke dealer di AS. Dua pekan lalu Toyota di AS mengumumkan penarikan 2,4 juta kendaraan di AS akibat cacat produksi pada pedal gas.Toyota juga menyatakan akan menarik 1,8 juta unit kendaraan di Eropa seminggu kemudian.

Full story

Menkeu Cabut Izin Asuransi Andhika Rahardja Putera

- Monday, February 8, 2010, 11:36

- Insurance News

- 1 comment

Jakarta - Menteri Keuangan Sri Mulyani melalui keputusannya No: KEP-84/KM.10/2010 tanggal 15 Januari 2010 mencabut izin usaha perusahaan asuransi kerugian bernama PT Asuransi Andhika Rahardja Putera (d/h PT Maskapai Asuransi Djakarta 1945).

Full story

Bapepam Revisi Aturan Baru Asuransi Kendaraan

- Monday, February 8, 2010, 11:34

- Insurance News

- Add a comment

Jakarta - Badan Pengawas Pasar Modal dan Lembaga Keuangan (Bapepam-LK) menerbitkan menerbitkan aturan baru tentang referensi unsur premi murni serta unsur biaya administrasi dan biaya umum lainnya pada lini usaha asuransi kendaraan bermotor tahun 2010.

Full story

Asuransi Kecelakaan Diri (Personal Accident)

- Saturday, January 30, 2010, 17:51

- Accident & Health, Personal Accident

- 17 comments

")

Property All Risks UKM (Usaha Kecil Menengah)

- Saturday, January 30, 2010, 17:49

- Commercial Package

- 14 comments

")

Property All Risks untuk Kantor

- Saturday, January 30, 2010, 17:42

- Property Insurance

- 6 comments

Property All Risks untuk Rumah Tinggal

- Saturday, January 30, 2010, 17:35

- Home Insurance, Home Package, Property Insurance

- 20 comments

Importance of shipping methods: Containers, Breakbulk and Bulk

- Thursday, January 28, 2010, 13:44

- Marine Cargo

- Add a comment

Containers & Loss Prevention of Goods in Containers

- Thursday, January 28, 2010, 13:32

- Marine Cargo

- Add a comment

Types of Containers

There are many and varied types of Containers which have been specifically designed for specialised jobs. Below and on the next few pages are descriptions of some of those more frequently used containers.

Ø General Purpose

Ø Open Top

Ø Flat Rack

Ø Insulated

Ø Refrigerated

Ø Bulk

Ø Open Sided

Ø Bolster

Ø Tank-tainer

Full story

Loss Prevention of Goods in Containers

- Tuesday, January 26, 2010, 22:01

- Marine Cargo

- Add a comment

Damage due to moisture and condensation of containerized goods

- Tuesday, January 26, 2010, 21:55

- Marine Cargo, Marine Cargo Insurance

- Add a comment

Since the transportation of containerized goods is usually covered at all-risk terms and conditions,

cargo insurers soon find themselves being called on to indemnify damage due to moisture and condensation. This is by far the main cause of losses in container traffic.

Containers are like scaled-down versions of a ship’s hold and are therefore subject to the same microclimatic conditions as those found on a conventional vessel. In the course of a long voyage, Full story

Standard Modes of Transport: FCL vs LCL

- Monday, January 25, 2010, 9:17

- Marine Cargo

- Add a comment

Machinery Breakdown and Boiler Explosion Clauses (Sub Limit ISR/PAR)

- Thursday, January 21, 2010, 11:36

- Property All Risks (PAR)

- 8 comments

Machinery Breakdown and Boiler Explosion Clauses (Sub Limit ISR/PAR)

Sub limit Machinery Breakdown dan Boiler Explosion adalah hal yang umum sekarang dilekatkan pada polis ISR/PAR alasannya apalagi jika bukan “menghemat premium”.

Bingung melekatkan klausul yang mana untuk sub limit MB dan Boiler??

Tempel saja polis MB dan PSAKI?

Or you may use these clauses….

Full story

Business Interruption on Influenza Pandemic

- Monday, January 18, 2010, 17:25

- Property Insurance

- Add a comment

SARS in 2003 had a severe impact on business activity in certain sectors of the economy (Hotels, Airlines, Travel and Health industries) mainly in Asia, a Flu Pandemic, with its greater contagion, is likely to hit the broader business communities globally.

"Business interruption” cover commonly exclude infectious diseases cover. However some underwriters may consider to allow extension on this infectious deseases.

Full story

Rating Composition

- Monday, January 18, 2010, 17:23

- Property Insurance

- Add a comment

A rate for a risk ideally should reflect the hazards and exposures that the risk presents. Similarly the broader the coverage the higher the rate should be.

A rate is made up of:

Full story

Moral Hazard

- Monday, January 18, 2010, 17:18

- Property Insurance

- Add a comment

Analysis of the moral risk does not only mean assessing the Insured's attitude to risk improvements or physical standards. It also includes what the client may do if he strikes financial difficulties or his behaviours when dealing with a claim.

Moral hazard can be one of the hardest aspects to judge. It’s also one of the most sensitive considerations you may be involved in.

Full story

Housekeeping and Fire Risk

- Monday, January 18, 2010, 9:30

- Property Insurance

- Add a comment

Fire and Allied Perils

- Monday, January 18, 2010, 9:19

- Property Insurance

- 3 comments

Fire implies the actual ignition of something which ought not to be on fire and it must be accidental or fortuitous as far as the insured is concerned. The fire need not originate in the insured premises, so if a fire occurs in a neighbouring premises and as a result damage by scorching or blistering is caused to the insured property, that would be recoverable under the policy. Other circumstances in which the loss is so closely connected with the fire that it is regarded as covered by the policy include:

Full story

Basis of Indemnity

- Monday, January 18, 2010, 9:17

- Property Insurance

- Add a comment

The policy wording will incorporate a definition of Indemnity under the title “Basis of Indemnity”. The way indemnity is calculated will vary depending upon what is insured. For example:

Buildings

The normal basis for buildings is the cost of repair or reinstatement. Adjustment may be necessary to compensate for “betterment”. This betterment can arise in two ways:

Full story

Sub Limits on IAR/PAR Policies

- Sunday, January 17, 2010, 11:28

- Property Insurance, Property Insurance

- Add a comment

Sub-Limits are imposed on IAR/PAR Policies to reduce the insurers liability for certain covers or to give extra extensions that are now very common included in the policy schedule

It is important that these be imposed for those type of perils or covers where it is inappropriate for the full policy limit(s) to apply. Remember that where no sub limit appears then the full sum insured is the limit.

Sub limits are now very common for the following covers:

Full story

Schering-Plough selesaikan kasus

- Sunday, January 17, 2010, 11:15

- Liability Casualty

- Add a comment

NEW JERSEY: Schering-Plough Corp mendapatkan izin penyelesaian kasus dari hakim untuk menutup gugatan pernyataan palsu kepada para investor mengenai obat alergi Clarinex.

Hakim Distrik AS Katharine Hayden di pengadilan federal Newark, New Jersey, memberikan persetujuan atas gugatan class-action yang melibatkan 280.000 investor. Perjanjian itu logis dan adil setelah tujuh tahun proses litigasi dan mediasi," ujarnya dalam putusan kemarin.

Full story

Broadcom bayar US$160juta

- Sunday, January 17, 2010, 11:14

- Liability Casualty

- Add a comment

FLORIDA: Broadcom Corp sepakat membayar US$160,5 juta tunai untuk menyelesaikan perkara gugatan dengan pemegang saham, terkait dengan praktik stock-option accounting yang dijalankan.

Sebagai kompensasi atas penyelesaian damai yang berhasil tercapai tersebut, sebagaimana dilaporkan Bloomberg, awal pekan ini, para pemegang saham selaku penggugat sepakat untuk membatalkan gugatan yang dilayangkan terhadap direksi dan komisaris perusahaan tersebut. Kendati telah tercapai penyelesaian damai yang berujung pada pencabutan gugatan tersebut, para penggugat dan tergugat tidak mengungkapkan secara detail poin-poin perdamaian yang dicapai kedua pihak. (BLOOMBERG/ELH)

Full story

Shell dihukum bayar denda

- Sunday, January 17, 2010, 11:12

- Liability Casualty

- Add a comment

LONDON: Shell UK Oil Products dan dua kontraktornya diganjar hukuman denda dengan jumlah total 283.000 pound sterling oleh Health and Safety Executive (HSE), terkait dengan kecelakaan di kilang minyak yang mencederai karyawannya.

Full story

Microsoft Ganti Rugi 180 juta US Dolar

- Sunday, January 17, 2010, 11:11

- Liability Casualty, Professional Indemnity

- Add a comment

IOWA- Pengadilan tinggi Iowa memutus Microsoft harus membayar ganti rugi 179,5 juta US dolar kepada warga Iowa, kemarin. Microsoft dinilai telah melakukan praktek monopoli dan anti kompetisi piranti lunak antara 1996 hingga 2006.

Full story

Membuat acuan bagi hakim hitung ganti rugi kasus HaKI

- Wednesday, January 6, 2010, 17:15

- News

- Add a comment

Selasa, 05/01/2010 00:00 WIB

Membuat acuan bagi hakim hitung ganti rugi kasus HaKI

Para penegak hukum sepakat perlunya peraturan sebagai acuan bagi hakim dalam membuat putusan nilai ganti rugi dalam perkara berkaitan dengan hak atas kekayaan intelektual (HaKI).

Kesepakatan tersebut diambil dalam satu workshop yang diselenggarakan oleh Tim nasional penanggulangan pelanggaran hak kekayaan intelektual di Bali pertengahan bulan lalu.

Full story

Other IMO Conventions

- Saturday, January 2, 2010, 16:30

- International Convention, Maritime Convention

- 2 comments

Other IMO Conventions

International Convention on Salvage, 1989 - 14/7/1996

The Convention replaced a convention on the law of salvage adopted in Brussels in 1910 which incorporated the "'no cure, no pay" principle under which a salvor is only rewarded for services if the operation is successful.

Full story

Maritime Safety Conventions: SOLAS, COLREG, STCW-F, SAR, SUA, Etc

- Saturday, January 2, 2010, 16:25

- International Convention, Maritime Convention

- 1 comment

Maritime Safety Conventions: SOLAS, COLREG, STCW-F, SAR, SUA, Etc

International Convention on Standards of Training, Certification and Watchkeeping for Fishing Vessel Personnel (STCW-F), 1995 - 7/7/1995

The Convention is the first attempt to make standards of safety for crews of fishing vessels mandatory. The revised Document for Guidance on Training and Certification of Fishing Vessel Personnel produced jointly by IMO and the Food and Agriculture Organization (FAO) and the International Labour Organization (ILO) takes into account the provisions of the STCW-F Convention.

Full story

Convention on Limitation of Liability for Maritime Claims (LLMC), 1976

- Saturday, January 2, 2010, 16:23

- Maritime Convention

- Add a comment

Convention on Limitation of Liability for Maritime Claims (LLMC), 1976

Adoption: 19 November 1976

Entry into force: 1 December 1986

Introduction

The Convention replaces the International Convention Relating to the Limitation of the Liability of Owners of Seagoing Ships, which was signed in Brussels in 1957, and came into force in 1968.

Full story

Protection & Indemnity (P&I) Cover

- Saturday, January 2, 2010, 8:04

- Protection & Indemnity, Protection & Indemnity (P&I)

- 1 comment

Cover")

{kind=link}

UK P&I Club – What is P&I?

- Friday, January 1, 2010, 10:32

- Protection & Indemnity

- Add a comment

UK P&I Club - What is P&I?

Shipowners insure against loss of or damage to their ships with hull underwriters. They look to the P&I Clubs for insurance against their liabilities to others.

These include their exposure to claims for damage or compensation in respect of the following heads of cover. The following description is a 'layman's guide' to the Rules of the Club and should not be treated as in any way definitive of the terms of cover provided. If you would like to see the full text of the Rules, please see Publications.

Full story

Collision Liabilities

- Friday, January 1, 2010, 10:29

- Protection & Indemnity

- Add a comment

Collision Liabilities

i. One-fourth collision liability

The English form of hull policy requires the ship's hull underwriter to pay three-fourths only of the liability of the insured ship in respect of loss or damage to another ship or her cargo as a result of the collision (subject always to the maximum mentioned under (iii) below). The remaining one-fourth of such liability is insured by the shipowners Club. This one-fourth usually makes the Club the largest single insurance interest, and in practice the managers of the Club will usually be asked by the hull underwriters to handle the issue of collision liability with the other ship and her cargo on behalf of all the underwriting interests. It is also usual for the Club concerned to give, on behalf of the insured shipowner, any necessary guarantees to the other ship and her cargo, the Club taking appropriate counter-security from the insured shipowner and also from the hull underwriters (or brokers) to the extent of their respective interests.

Full story

The International Group of P&I Clubs

- Friday, January 1, 2010, 10:28

- Protection & Indemnity

- Add a comment

The International Group of P&I Clubs

The International Group of P&I Clubs exists to arrange collective insurance and reinsurance for P&I Clubs, to represent the views of shipowners and charterers who belong to those Clubs on matters of concern to the shipping industry and to provide a forum for the exchange of information.

Full story

- Polis Standar Asuransi Komprehensif Harta Benda Indonesia 564 comments

- Mengapa banyak perusahaan rugi di lini bisnis asuransi kapal? 423 comments

- Bagaimana cara membatalkan polis asuransi? Apakah kena denda atau pinalti? 215 comments

- Asuransi Pengangkutan Barang (Marine Cargo Insurance) 181 comments

- Telat bayar premi: Apakah polis otomatis batal? 110 comments

- Asuransi Kapal dan P&I (Marine Hull and P&I) 87 comments

- Asuransi Pekerja: Jamsostek, Workmen Compensation, Personal Accident vs Employers Liability 83 comments

- Asuransi Kerugian 76 comments

- Very Important Clauses : Klausul-Klausul Penting dalam Asuransi Kebakaran (Fire & Property Insurances) 68 comments

- Asuransi Property All Risks (PAR) / Industrial All Risks (IAR) 52 comments

- Neon Sign / Billboard Insurance 51 comments

- Prosedur Klaim Asuransi Kerugian: Asuransi Harta Benda (Property Insurance) 49 comments

- Indemnity vs Reinstatement 48 comments

- Motor Vehicle Insurance - Quotation 45 comments

- Asuransi Kendaraan Bermotor 44 comments