What Changes on Property Rate in Indonesia after New OJK Tariff Regulation?

- Saturday, August 2, 2014, 8:17

- Insurance News

- 6 comments

Please download pdf version here for your happy reading :

What Changes on Property Rate in Indonesiaafter New OJK Tariff regulation?

Effective as at 1 February 2014, The Indonesian Financial Services Agency (OJK) has instructed all insurance providers in Indonesia to apply a mandatory tariff for property insurance, full document is available for download with link provided at the bottom of this article. The purpose of this article is to give short summary on Structure of the New OJK Tariff and the Impact on Property Class of Business.

1) New OJK Tariff – Structure

- Effective as at 1 February 2014

The draft was first circulated publicly on Dec. 24, 2013, and implemented on Feb. 1, 2014 for all new policies and renewal policies with period of insurance on or after Feb. 1, 2014 irrespective of date of issue.

In order to prevent unfair conduct amongst the insurance companies, OJK later issued a circulation that prohibit customers to change period of insurance of the existing policies to period prior of Feb.1, 2014 or cancel the policies from existing carriers and move to other carriers to save the premium prior implementation of this regulation prior to Feb. 1, 2014

- Rated as per “Code of Occupation” and “Class of Construction”

The new rate scheme classifies properties into 120 types of Occupation of the buildings including industrial, commercial and residential and further graded down as per Class of Construction 1, 2 or 3. Although the new scheme does not classify property rate as per Fire Protection but the new rule set the maximum and minimum premium rates, you cannot sell it lower than minimum rate or higher than maximum rate, but you can sell it with rate in-between.

- Rate for FLEXAS, FTSWD and EQVET are Tariff

The new rule set the maximum and minimum premium rates chargeable for FLEXAS (fire, lightning, explosion, aircraft impact and smoke) coverage with rates based on industrial risk codes, for FTSWD (flood, including typhoon, storm and water damage) coverage with rate based on 4-flood zones and 2-areas according to their potential risk of flood, EQVET (earthquake, volcanic eruption and tsunami) coverage with rate set on 4-earthquake zones. The tariff has to be uniformly applied, irrespective of wordings used.

For the purpose of compliance or audit OJK warrants that rate for each perils shall be brokendown under the policy, rate shall be based on OGR (original gross rate), net rate is not allowed.

- Rate for RSMDCC and OTHER Perils are non Tariff (Not regulated)

It provides, additionally, discretionary loadings to balance coverage for RSMDCC (riots, strikes and malicious damage, and civil commotions) theft and accidental damage (OTHERS), these perils are not tariff. This provides room for insurance company to compete.

- MB is rated separately (non-Tariff)

Prior to implementation of this new OJK tariff, it was a market practice to give Machinery Breakdown (MB) Sub-limit under Property Policy for free, and it is now prohibited, MB shall be rated separately (but non-tariff) and issued under separated MB policy (except for a multi-peril policy for large risks only, MB can be included)

- Minimum DEDUCTIBLES for FLEXAS, FTSWD, EQVET and BI are regulated

The tariff also impacts deductibles. Heavy industrial risks attract a minimum FLEXAS deductible of 5 percent of recoverable claims or 0.1 percent of the sum insured/declared value (per location), whichever is higher. New earthquake deductibles are set at 2.5 percent of the total sum insured, with a maximum of $3 million, while the flood deductible is 10 percent of a recoverable claim. Business interruption deductibles range from 14 to 30 days (seven days for floods) and are generally below international norms for individual risks.

- First Loss Limits are allowed and rated as per Scale

Property Insurance (cover for FLEXAS, FTSWD, EQVET, RSMDCC, OTHERS) including BI and MB and LOP MB (Loss of Profit following Machinery Breakdown) can be arranged on First Loss Limits irrespective of the Sums Insured and rated as per Scale provided in the new scheme.

- TSI exceeds USD 300 m is rated 50% off (including MB)

Flexibility is offered for large risks where asset values (or Total Sums Insured (TSI)) at a single location exceed $300 million. Here insurers are permitted to apply 50 percent of the mandatory tariff rates, flexibility also to include Machinery Breakdown (MB) cover for free, but tariff deductibles still apply

- Brokerage/Commission is max.15% (+VAT)

This what makes broker and agent are very un-happy about, their commission is cut to maximum 15% only while previously they enjoyed 20% to 50%

- Reinsurance Commission is max.27.5% (+VAT)

Reinsurance commission on proportional treaty and facultative is set at maximum 27.5%. Reinsurance rate shall be based on OGR (original gross rate), net rate is not allowed

- NCD : 5% only

No Claim Discount (NCD) is set at maximum 5% only provided no claim on preceeding year (and not in accummulative), apply for renewal period after Feb. 1, 2015 or one-year after application of this new OJK Tariff.

2) Impact of New OJK Tariff on Property Class of Business

- Comparison “Before & After”

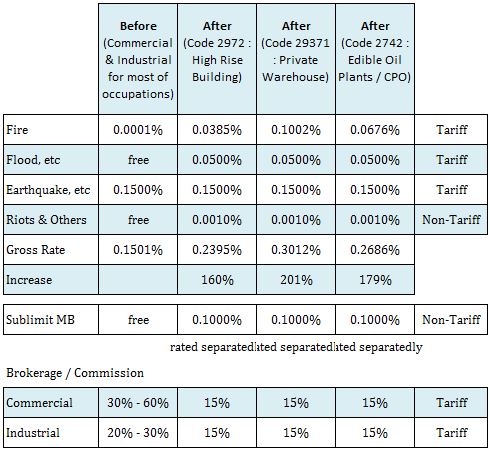

New and renewal insurance policies for property risks, as per immediately, will see a number of restrictions in coverage as well as premium increases between 50 percent and 350 percent, here are some comparison “Before & After” implementation of new OJK tariff:

Before

Prior to implementation of New OJK Tariff, for most of occupations, commercial buildings or industrial risks were rated at Earthquake rate (0.1500%) plus 0.0001% Fire rate, Other perils were free, including Machinery Breakdown (MB) sub-limit for free, making worse with 20% to 60% brokerage/ commission.

After

As per new OJK Tariff structure set out above, each peril is rated separately, MB rated separately thus Gross Premium increases 100 to 350 percent, with brokerage / commission cut to maximum 15%, it’s absolutely a very fantastic increase on side of insurance company and a very worse scenarion on site of customers (client).

- Selling @ minimum rate

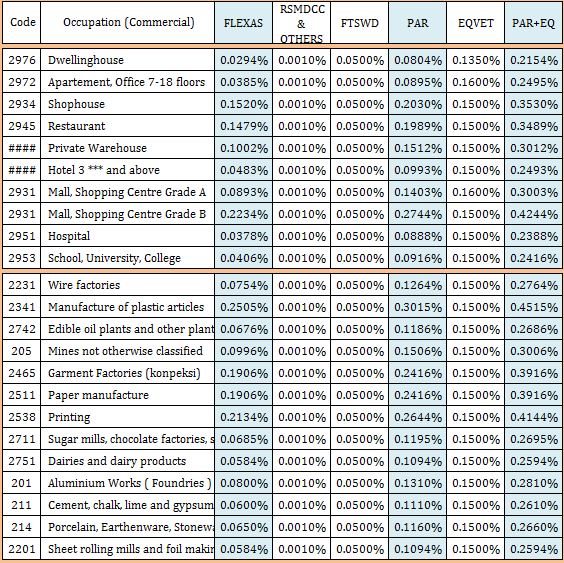

Eventhough the new rule set the maximum and minimum premium rates chargeable, but every one selling at minimum premium rate for competitive reason, no one selling higher than minimum rate except for “un-acceptable risk”, thus the premium rates for some residential, commercial and industrial risks would likely be seen as follow:

- Restriction in Coverage

Because the premium increase is “fantastic”, this leading to higher overall costs of doing business for all businesses operating in the country, clients or brokers are now to find alternative either to restrict the coverage of arrange a “first loss limit insurance”.

You may be seen above EQVET rate contributes about 50% of the total premium, clients at considerably “earthquake-safe” areas may consider to take-out EQVET cover and saving 50% insurance cost, clients at “non-flood-prone” areas may further take-out FTSWD cover to save further 0.0500% premium, and the worst scenario is to take Fire cover only.

- Alternative placement : Proportional v XoL Reinsurances

The new Scheme sets maximum brokerage / commission : 15% and reinsurance commission at maximum 27.5%, alternatively insurance companies or reinsurace brokers are now arranging XoL reinsurance for their large accounts, XoL reinsurance placement is not subject to this regulation

- Premium Growth v Profitability

With very-adequate premium on property class of business, it is time for insurance companies to grow their property portfolio and maintain profitability, some of them are now open for ‘high risk’ accounts i.e. plastic, plywood, paper, chemical manufacturing risks or retain small portion and reinsure-out large portion out-there reinsurers are happy to accept with new-premium-increase-rule.

- Brokers are working cost-effectively

On the other hand, brokers are now working cost-effectively, because property rate is now go tariff no-much room to negotiate with underwriters, brokerage reduces to 15%, alternatively brokers are now seeking e-placement (electronic-based-platform) or seeking so-called a ‘portfolio-transfers’ from existing carriers (not to mention domestic insurance companies with little comfort on financial strength) to carriers with international reputation with ‘A-rated papers’ joint-venture insurance companies.

It shall be noted the new property rates may not 100% ideal some occupations in particular mining, heavy industrial risks and the like are lower than rates for warehouses or shop-houses, the new property rates are said to be built based-on 10-years BPPDAN books and worked by independent actuary hired from reputable universities i.e. ITB, IPB, UGM and UI

OJK warrants that violation against this regulation will carry serious penalty, regular audit will be held to assure compliance.

Good Luck !

Imam MUSJAB

Qualified Insurance Practitioner

Full Document concerning the new OJK tariff is available on pdf format here:

English version (translation) of the document is available upon request, for any inquiry please give me a call at +628128079130 email at imusjab@ahliasuransi.com or imusjab@gmail.com

About the Author

IMAM MUSJAB has written 1869 stories on this site.

6 Comments on “What Changes on Property Rate in Indonesia after New OJK Tariff Regulation?”

Write a Comment

Gravatars are small images that can show your personality. You can get your gravatar for free today!

Pak imam terkait biaya akuisisi max 15% apakah handling fee yg diterapkan oleh leader tidak termasuk di dalam biaya akuisisi. Contoh apabila ada leader asuransi menerapkan outgo 15% plus handling fee 2,5% apakah hal inidiperbolehkan oleh ojk. Terima kasih

Handling Fee 2.5% Leader adalah ditagih ke member termasuk dalam maksimum 27.5% (R/I Comm), Jadi total tidak boleh lebih dari 27.5% – Bukan Direct Comm / Brokerage

Jadi intinya tidak menyalahi aturan ojk ya pak jika diterapkan outgo 15% dan handling fee 2,5% ?

Melanggar aturan maksimum biaya akuisisi 15% – tidak boleh

Dear Pak Imam

Saya mau nanya untuk kategori pabrik karung plastik apakah bisa masuk dalam kategori sackmakers (2451)???, mengingat bahwa kalau dikode 2341 merupakan manufacture of plastik article.

Terima kasih atas jawabannya.

Salam

Puji Atmojo

Kayaknya 2451 bukan karung atau kantong plastik, Pak kalo materialnya dari plastik masuk 2341

Saya mau tanya Pak…untuk Tarif RSMDCC untuk asuransi PAR apakah ada minimun dan maksimum tarifnya? ataukah setiap asuransi boleh menentukannya sendiri? ataukah ada batas wajar tarifnya dari OJK?

Terima Kasih.

TIDAK DIATUR. Biasanya berkisar 0.0001% s/d 0.001%

75xuht

tku641